Quick takeaway

Gold is receiving an inflation warning without the usual inflation-hedge payoff. Markets are increasingly treating higher prices as a reason for tighter monetary policy, leaving non-yielding bullion under pressure.

What happened

Gold is getting plenty of inflation. It is not getting the rally that usually comes with it.

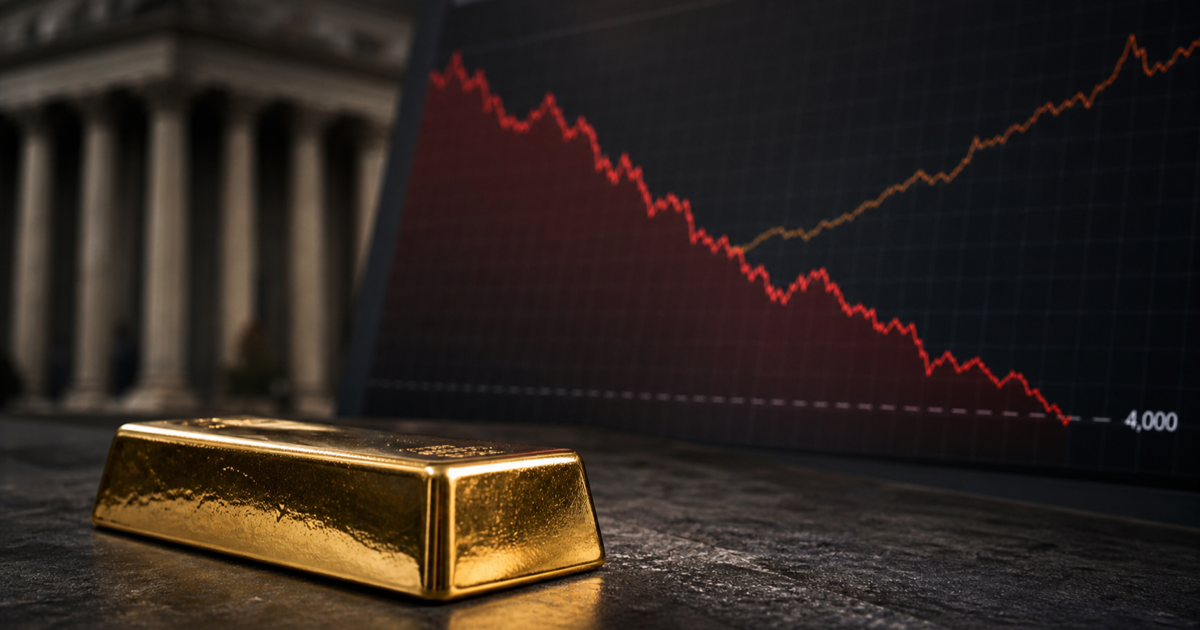

Bullion traded near $4,080 an ounce on Thursday, close to its lowest level since early November and roughly 27% below January's record. Prices found a little stability after Wednesday's sharp fall, but the latest economic news gave buyers no convincing reason to return.

The U.S. producer price index rose 1.1% in May, the Bureau of Labor Statistics reported, matching April's upwardly revised monthly increase. Producer prices were 6.5% higher than a year earlier, the fastest annual pace since November 2022.

Energy did most of the damage. Final-demand energy prices jumped 10.7% in one month, while gasoline surged 23.4%.

Those numbers matter because producer prices often show cost pressure before it reaches consumers. Companies can absorb some of that increase through lower margins, but a shock this large raises the risk that more expensive fuel, transport and materials eventually appear in retail prices.

On another day, that might have strengthened the case for gold as protection against inflation.

Instead, it strengthened the case for higher interest rates.

Why it matters

The European Central Bank underlined that shift by raising its three key policy rates by 25 basis points on Thursday. It was the ECB's first increase since 2023. The bank said the war in the Middle East had disrupted energy supplies and pushed inflation sharply higher, forcing policymakers to act despite a weaker economic outlook.

The ECB's move is important well beyond Europe. It shows how quickly the global policy conversation has changed. Investors entered 2026 expecting easier monetary conditions. They are now considering whether an energy-driven inflation shock could make central banks tighten again.

That is a difficult backdrop for gold.

Bullion pays no interest, so it tends to become less attractive when cash and government bonds offer higher returns. Inflation can still help gold, but usually when it damages confidence in currencies or pushes real interest rates lower. When inflation instead produces rate hikes and higher bond yields, the relationship can work in reverse.

Thursday's market is a clear example. Producer inflation reached a multi-year high and a major central bank raised rates, yet gold remained pinned near a seven-month low.

The contrast also explains why geopolitical tension has failed to deliver a lasting safe-haven rally. Conflict around Iran and the Strait of Hormuz has lifted oil and increased economic uncertainty. But traders are looking through the immediate fear trade and focusing on the policy consequences: higher fuel costs, stubborn inflation and fewer rate cuts.

For gold, the next major test is now uncomfortably close.

The psychological $4,000 level sits less than 2% below Thursday's price. A move toward that area would deepen the valuation reset that began after January's peak and could attract longer-term buyers. It could also trigger another round of selling if investors treat a break below $4,000 as confirmation that the downtrend still has room to run.

The longer-term case for gold has not disappeared. Central-bank demand, reserve diversification and geopolitical risk remain meaningful supports. But those forces are being asked to compete with a market that is suddenly repricing the path of global interest rates.

That is today's striking valuation story: gold is not falling because inflation has vanished. It is falling because inflation has become severe enough to make tighter policy credible again.

What to watch next

The first signal is whether gold can recover above $4,200, the level it broke on Wednesday. A rebound through that area would suggest the latest selloff is becoming stretched. Continued trading below it keeps the $4,000 test in view.

The second signal is the bond market. If Treasury yields climb as investors price a more hawkish Federal Reserve, gold may remain under pressure. If yields retreat because growth concerns begin to dominate, bullion could regain some defensive demand.

Oil is the third piece. Another sharp energy move would intensify the inflation problem, but it would not automatically help gold. The market's reaction will depend on whether investors fear the conflict itself or the rate hikes that expensive energy may produce.